According to Census Bureau data from 2025, the median annual household income for Americans aged 65 and older is $56,680. It’s higher for households aged 65–74 ($61,000 to $69,000) and lower for households aged 75 and older ($47,790).

The average figures, pulled up by a smaller number of high earners, run roughly 50% above each median, which is why the median is the more useful benchmark.

| Income Per Year | Median | Mean |

|---|---|---|

| Households 65-69 Years Old | $68,860 | $102,000 |

| Households 70-74 Years Old | $61,780 | $92,600 |

| Households 75+ Years Old | $47,790 | $73,820 |

But the harder question is whether your own income will last as long as you do, and if you’re short of where you want to be, what’s going to fill the gap. This page covers the full breakdown of where retirees’ income comes from, then walks through a retirement gap worksheet to figure out your specific shortfall and what it would cost to cover with guaranteed lifetime income.

Why the Average Doesn’t Tell You What You Need To Know

Two retired households can have identical incomes and very different financial situations. A couple pulling $75,000 a year from a defined-benefit pension and Social Security is in a different position than a couple pulling $75,000 a year from portfolio withdrawals, even though the income line on the tax return looks the same. The first couple has guaranteed income for life. The second couple has income for as long as the portfolio holds up.

The same goes for whether you’re “on track.” If your target retirement income is $80,000 a year and you’ll have $30,000 from Social Security, the gap you need to fund yourself is $50,000 a year, every year, for the rest of your life. The average doesn’t help you size that number. The worksheet below does.

Figuring Out Your Retirement Income Gap

This four-line formula gives you the income shortfall you’ll need to cover from savings; the number that actually drives most retirement decisions.

- Line 1: Your target retirement income

- A common starting point is 75–85% of your final pre-retirement salary. So, if you’ll be earning $90,000 in your last working year, your target is roughly $67,500–$76,500 a year in retirement. Adjust upward if you plan to travel heavily, support adult children, or face higher healthcare costs. Adjust downward if your mortgage will be paid off and your essential expenses will drop.

- Line 2: Subtract your expected Social Security

- Pull your most recent benefit estimate from your my Social Security account at ssa.gov/myaccount — the estimate is personalized to your earnings record and your planned claiming age. The 2026 average benefit for retired workers is approximately $1,976 per month, or $23,712 per year. The maximum at full retirement age is approximately $4,018 a month, and waiting until 70 increases it further. Use your actual estimate, not the average.

- Line 3: Subtract any pension income

- Only about one in three retirees has a defined-benefit pension. If you do, use your plan’s projected benefit at your planned retirement date. The median private pension currently pays approximately $10,606 per beneficiary per year, but yours may be substantially higher or lower.

- Line 4: What’s left is your gap

- Target − Social Security − Pension = the income shortfall you need to cover from savings every year, for the rest of your life. For most retirees without a pension, the gap runs $20,000–$40,000 a year.

What It Costs to Fill the Gap

This is the question the benchmark tables can’t answer. Once you know your gap, you can price the most direct way to fill it: a single-premium immediate annuity (SPIA) that converts a lump sum into guaranteed income for the rest of your life.

At current rates, here is approximately what it takes to generate $2,000 a month in lifetime income, a $24,000-a-year gap, starting at age 65:

- Single-life SPIA, male age 65: approximately $320,000

- Single-life SPIA, female age 65: approximately $340,000 — slightly higher than the male equivalent because of longer life expectancy

- Joint-life SPIA, couple both age 65: approximately $375,000 — pays for as long as either spouse is alive

Figures based on prevailing April 2026 SPIA payout rates. Actual quotes vary by insurer, state, and rate environment; pricing refreshes quarterly.

If you have liquid savings to cover ages 65–75 from a portfolio, a deferred income annuity (DIA) with payments starting at 75 instead of 65 costs significantly less upfront; the insurer earns ten years of mortality credits before payments begin. For longevity-focused retirees, that’s often the more efficient way to lock down lifetime income for the back end of retirement.

An important caveat. The lump sum is no longer accessible once annuitized. Annuitization buys guaranteed income at the cost of liquidity, so most planners recommend annuitizing the portion of savings needed to cover essential expenses, not the full balance.

Anna and Phil were in their 50s and wanted to plan for their perfect retirement, defined by low risk and certainty. When they approached me, I had to tell them what I’m sure they already knew: “I cannot predict the future, but I can make educated decisions for you, and right now the best strategy to plan for retirement income is truly to diversify your sources of income.”

In Anna’s case, she was expecting an inheritance and to sell her business in the next 10 years. In Phil’s case, he was expecting to retire from his law practice and sell the piece of land he had bought as a bachelor several years ago. They both decided to start a consulting business on the side to cover their fixed expenses and use their passive income to fund their traveling adventures. It is possible with a mix of investments, rental income, consulting fees, and annuities.

Elaine King, MBA, CFP®, CDFA™, CFBA, ACCFounder of Family and Money Matters™Elaine King, CFP®, founder of Family and Money Matters™, empowers families’ financial and human capital for wellbeing. She’s crafted actionable plans for 1,200+ families and 100+ enterprises. A recognized financial education advocate, creator of LATAM’s first family financial program and winner of the Best Latin Book Award. Featured in top publications and honored by Investopedia and People Magazine.

What Inflation Does to Your Gap

A $24,000-a-year gap at 65 isn’t a $24,000-a-year gap at 85. At 3% inflation, $24,000 today buys roughly $32,000 worth of goods in 10 years and approximately $43,000 worth in 20. Any plan that fixes nominal income at one age erodes in real terms across a long retirement.

Three structural ways to handle this. A SPIA with a COLA rider pays a smaller starting check that grows at a fixed annual rate, protecting purchasing power at the cost of upfront income. A staggered SPIA strategy buys multiple smaller annuities over time, repricing into higher rates as you age. A fixed-indexed annuity ties credited interest to an index with downside protection, accepting more variability in exchange for inflation-responsive growth. Each fits a different risk preference.

Average Retirement Savings by Age Group

Saving for retirement can begin at any age, but the most robust retirement plans are associated with aggressive savers that started early, oftentimes, in their early 20s. Unfortunately, life circumstances prevent many people from saving for retirement until their 30s, 40s or 50s.

Starting to save for retirement later in life is challenging, but you can do it successfully. It just requires careful planning and persistence. When starting at age 50 or older, it also usually calls for some sacrifices and more stringent retirement budgeting.

Not all individuals take the traditional path to retirement. Depending on your income level, savings rate and anticipated spending needs, you may be able to retire early. However, saving for retirement is challenging enough; early retirement calls for superb planning and a heightened level of fiscal discipline.

Vanguard conducted a study to examine how America saves. The mean and median retirement savings by age group are as follows:

Average Retirement Savings by Age Group

| Age Range | Average Balance | Median Balance |

|---|---|---|

| 0-25 | $6,264 | $1,786 |

| 25-34 | $37,211 | $14,068 |

| 35-44 | $97,020 | $36,117 |

| 45-54 | $179,200 | $61,530 |

| 55-64 | $256,244 | $89,716 |

| 65+ | $279,997 | $87,725 |

How do you fare relative to the median for your age group? If you’re lagging considerably, perhaps it’s time to meet with a financial advisor. Doing so will improve your chances of accumulating enough savings to generate an adequate amount of income in retirement.

Where Does Retirement Income Come from?

Many people have various sources of retirement income, which can include pension plan distributions, Social Security benefits and investment account distributions. Ideally, you should have multiple, diverse streams of income to ensure you have enough to live comfortably, optimize your tax position and protect against inflation. Let’s take a closer look at the most prominent sources of retirement income.

Continued Employment

According to a recent study by Schroders, 62% of working Americans plan to continue working during retirement in some capacity. Fortunately, there does not appear to be a shortage of work. In fact, there are a wide variety of opportunities for retirees to make money and grow their skills — from keeping a blog to becoming a life coach.

How to maximize this income:

- Start a freelance consulting business using the skills you honed throughout your career.

- Get a part-time job.

- Utilize gig-economy to find something flexible that aligns with your lifestyle.

Social Security Benefits

Every time someone gets paid, a 6.2% Social Security tax is withdrawn from the gross amount. For the self-employed, this percentage doubles to 12.4%. Then, the Social Security program pays this money to qualifying retirees, including you. The amount you receive is based on how much you earn during your working years and the age you elect to start your benefit.

A study conducted by the National Institute on Retirement Security shows that 40% of Americans rely solely on Social Security benefits to fund their retirement.

According to the Social Security Administration, for 2022, the maximum Social Security benefit you can receive each month is $3,345 for those at full retirement age. The estimated monthly average Social Security income is $1,657, after a 5.9% cost-of-living adjustment.

How to maximize this income: Delay receiving your Social Security benefit until full retirement age, which is between 66 and 67, depending on when you were born. Claiming the benefit prior to full retirement age will result in a reduced monthly payment. Brian Fry, a CERTIFIED FINANCIAL PLANNER™ and founder of Safe Landing Financial, offers the following guidance:

“To receive 100% of your Social Security benefit, you must wait until full retirement age. Each year that you claim before full retirement age, you give up between 5% and 6.67% of your full benefit. Benefits increase by approximately 8% for each year that you delay claiming Social Security after full retirement age.”

What If the Market Drops the Year You Retire?

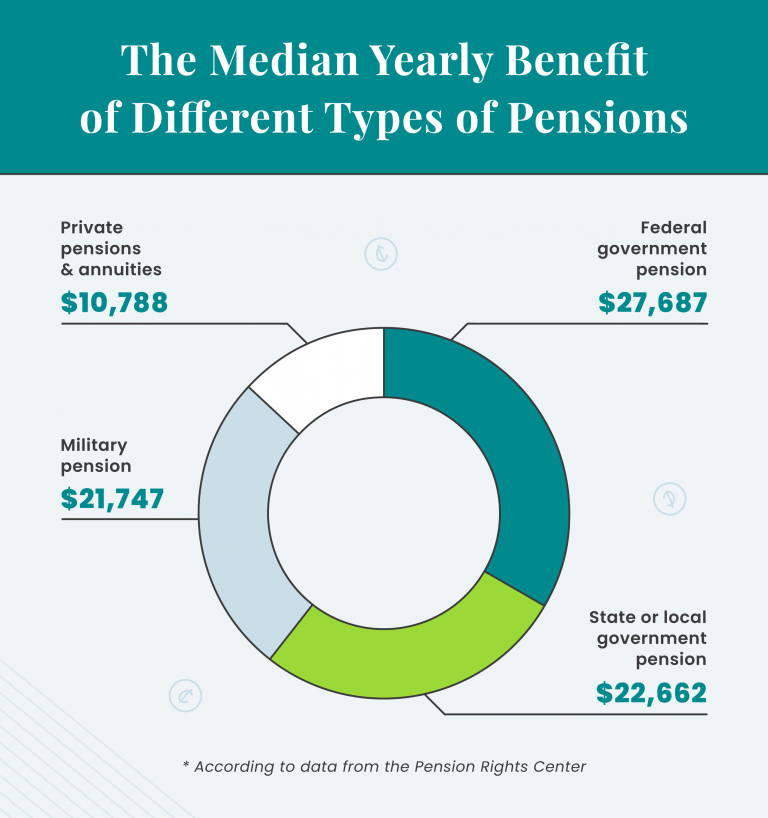

Pensions

According to the Pension Rights Center, only about one-third of American retirees receive income from defined benefit retirement plans, which reflects the steady decline in pension plans. According to the United States Department of Labor, there were 113,062 pension plans in 1990, but only 46,869 in 2018.

The median private pension in the United States pays out $10,606 per beneficiary annually, according to the latest data from the Pensions Rights Center. On average, other types of pensions, including government and military pensions, pay out higher benefits.

How to maximize this income: Generally, by working as long as possible for a pension plan sponsor, you can increase your benefit. Usually, the benefit will also increase as you earn more money.

Personal Financial Assets

According to the Transamerica Center for Retirement Studies, 48% of American workers expect their main form of retirement income to be from personal financial assets, some of which, are tax-advantaged.

Most investors hold some combination of the following assets:

- Annuities

- IRA accounts

- 401(k) accounts

- Taxable brokerage accounts

- Real estate

Depending on how they’re structured, the first three vehicles offer the potential for either tax-deferred or tax-exempt growth. The latter two asset types do not receive favorable tax treatment.

Regardless of the personal financial assets you own, strive to maintain a holistic perspective. The success of your retirement plan is dependent on how the various assets complement each other and your other sources of income, not on standalone performance. Along those lines, be sure to strive to maintain an appropriate degree of diversification. This can help to improve the risk-adjusted performance of your retirement portfolio and extend the longevity of your savings.

-

“As a baby boomer approaching retirement age, I find myself doing general research to reaffirm some strategies that we have worked on since our early thirties. We feel comfortable that, at this time, my income streams will support the lifestyle and projected health care costs for me and my spouse. That is with the full understanding that we cannot plan for every contingency — but confident and reassured in the plan we’ve made. Informative article indeed, thanks.”ELLIOTT ROSSAnnuity.org Reader

“As a baby boomer approaching retirement age, I find myself doing general research to reaffirm some strategies that we have worked on since our early thirties. We feel comfortable that, at this time, my income streams will support the lifestyle and projected health care costs for me and my spouse. That is with the full understanding that we cannot plan for every contingency — but confident and reassured in the plan we’ve made. Informative article indeed, thanks.”ELLIOTT ROSSAnnuity.org Reader

How to maximize this income:

- Invest the maximum amount into your retirement accounts each year.

- Look into buying an annuity to protect your savings and grow your money on a tax-deferred basis. In doing so, be sure to shop around for reputable annuity providers.

- Invest your money in passive, income-producing investment funds that hold bonds, dividend-focused stocks and commercial real estate.

4 Withdrawal Strategies for Retirement Income

Building adequate sources of income is one aspect of the retirement journey. Being strategic about the way you withdraw funds during retirement is the other. Without a solid plan, you may spend too much too fast and not have enough money to support your lifestyle. Fortunately, the strategies outlined below can help you extend the longevity of your savings.

- Annuities: An annuity is a tax-deferred financial product issued by an insurance company. To buy an annuity, you typically pay the issuer a lump sum of money in exchange for a guaranteed stream of income. However, this payment may also be made over time, and the income period can vary based on the terms of the annuity.

- The 4 percent rule: This rule suggests you should withdraw 4% of your retirement portfolio in the first year of retirement and adjust for inflation in subsequent years. Doing so can help preserve your capital.

- Fixed-percentage or fixed-dollar withdrawals: With this approach, you determine a specific percentage or amount to withdraw periodically. Projections are necessary to hone in on an appropriate withdrawal.

- The Bucket Method: With this system, you divide your money into distinct buckets that serve specific purposes. Some of your funds will remain in a liquid bank account to cover day-to-day expenses. Other funds may be invested in relatively stable, fixed-income assets to generate income to replenish your bank account. Other funds may be invested in growth-oriented assets to bolster the value of your retirement portfolio.

Don’t underestimate the importance of maintaining a strategic distribution plan. It can make the difference between having a stressful, uncertain retirement and living comfortably and confidently. If you’d like to explore these approaches in more detail, consult with a fiduciary financial advisor.