If you retire under the Federal Employees Retirement System (FERS) before age 62, you may qualify for the FERS Annuity Supplement, also called the Special Retirement Supplement (SRS). This benefit provides extra monthly income meant to replace the Social Security you’re not old enough to receive yet.

In other words, if you meet FERS early-retirement requirements, you’ll receive your regular FERS pension, plus this supplement, until you turn 62. After that, the supplement stops and Social Security becomes your next source of income.

Eligibility rules and earnings limits can affect how much you receive, so understanding how the supplement works is important when planning your retirement.

Legislative Update — June 2026: The House passed H.R. 1 (the “One Big Beautiful Bill Act”) in 2026. If signed into law, it would eliminate the FERS annuity supplement for certain employees effective January 1, 2028. The bill has moved to the Senate, where federal employee unions including the APWU are actively lobbying against it. If you are considering early retirement and expecting to receive the supplement, factor this uncertainty into your timing. Employees who begin receiving the supplement before January 1, 2028 may be grandfathered, but that outcome is not guaranteed as of this writing.

Who Qualifies for the FERS Annuity Supplement

| Retirement Type | Qualifies? | Notes |

| Immediate unreduced FERS pension (before age 62) | Yes | Primary qualifying path for most FERS employees |

| MRA+10 postponed benefit | No | Supplement not payable on postponed benefits |

| Deferred retirement | No | Not eligible regardless of years of service |

| VERA/VSIP early retirement | Conditional | Eligible, but supplement doesn’t begin until you reach your MRA |

| Special category (LEO, firefighter, ATC) | Yes | Eligible at age 50 with 20+ years; earnings test exemption until MRA |

| Disability retirement | No | Not payable under disability retirement provisions |

How the FERS Supplement Is Calculated — and What You Might Get

The FERS supplement is intended to approximate the Social Security benefit you earned during your federal employment. The amount is determined using a formula that takes your years of FERS-covered civilian service and estimates what your Social Security benefit would have been at age 62.

How to Estimate Your FERS Supplement — Step by Step

Step 1: Log into SSA.gov and find your estimated Social Security benefit at age 62. Use the “age 62” number on your statement — not the full retirement age figure.

Step 2: Count your years of FERS-covered civilian service. Use whole years only. Military time does not count unless you made a formal deposit to credit it.

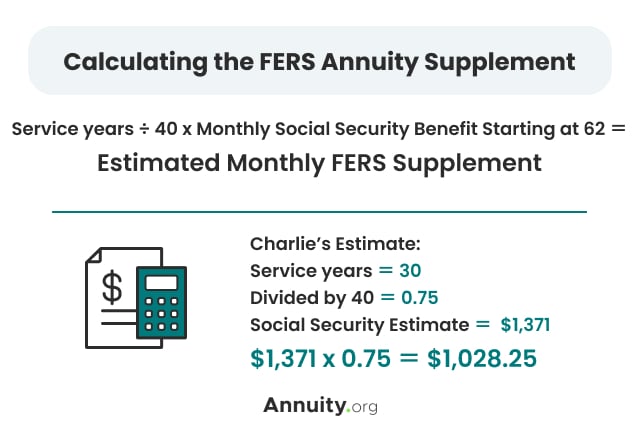

Step 3: Apply the formula — (Years of FERS service ÷ 40) × Estimated Social Security benefit at age 62 = Your monthly supplement estimate.

| Variable | Example |

| Years of FERS service | 28 years |

| Estimated Social Security benefit at 62 | $1,800 / month |

| Calculation | 28 ÷ 40 = 0.70, then 0.70 × $1,800 |

| Estimated monthly supplement | $1,260 / month |

Note: OPM calculates your official supplement amount when you file for retirement using your actual Social Security earnings record. This formula gives a reliable estimate but your final figure may differ slightly.

Because the supplement mimics Social Security, it’s reduced if your retirement earnings exceed a certain threshold. For example, extra earned income (from a part-time job or self-employment) could reduce or even cancel the supplement.

How the FERS Supplement Works (At a Glance)

- The supplement fills the income gap between early retirement and Social Security.

- To receive it, you must retire under FERS before age 62 with an immediate, unreduced annuity.

- Amount is based on your years of service and estimated Social Security benefit at age 62.

- It ends when you turn 62 or begin Social Security — and extra income in retirement can reduce it.

When the FERS Supplement Ends

The FERS supplement doesn’t last forever. In nearly all cases, it ends at the end of the month before you turn 62, or just before you start receiving Social Security benefits.

Because of that, if you retire early, it’s best to plan ahead: know how much your basic FERS pension will be on its own, and make sure you have enough saved or invested to cover living expenses once the supplement stops.

Potential Pitfalls — What Could Reduce or Eliminate Your Supplement

Your FERS supplement can disappear more easily than many retirees realize. If you retire under a deferred or postponed benefit instead of an immediate, unreduced pension, you generally won’t qualify for the supplement at all. Even if you do qualify, the payment may shrink if you earn too much income after retiring. Wages and self-employment earnings count toward the annual limit, and anything you earn above that limit reduces the supplement — in some cases wiping it out completely.

| Detail | 2026 Amount |

| Annual Earnings Limit | $24,480 (up from $23,400 in 2025) |

| Reduction Formula | $1 reduction for every $2 earned above the limit |

| Income That Counts | Wages, salary, self-employment income |

| Income That Does NOT Count | TSP withdrawals, rental income, investment income, pension payments |

| Special Category Exemption (LEO/FF/ATC) | Exempt from the earnings test until reaching their Minimum Retirement Age (MRA) |

The supplement also ends automatically once you turn 62 or become eligible for Social Security, even if you decide not to claim Social Security right away.

Example: A 58-year-old retiree takes an immediate FERS pension and qualifies for the supplement. She later picks up consulting work that pushes her income above the earnings limit. Her supplement is reduced month by month until, eventually, it drops to zero.

Who Benefits from the FERS Supplement

The FERS supplement is most valuable for employees who retire early with many years of federal service, and those who rely heavily on their FERS pension for income. It’s especially helpful for special-category employees, such as law enforcement officers, firefighters and air-traffic controllers, who often retire in their 50s and can begin receiving the supplement right away.

It also benefits anyone who wants to bridge the gap between their FERS retirement date and the start of Social Security, helping them maintain steady income without drawing down savings.

Example: A 57-year-old law enforcement officer retires with 25+ years of service. The supplement provides Social-Security-like income immediately, covering the years until he turns 62 and becomes eligible for actual Social Security.

- Weekly Rates.

- Delivered Every Monday.

- Always Free.

How To Use the FERS Supplement in Your Retirement Plan

The FERS Annuity Supplement can be an important part of a federal retiree’s income strategy, but only if you understand when it applies, how it’s calculated, and when it ends.

If you’re eligible for an immediate, unreduced FERS pension and retire before 62, the supplement gives you a built-in bridge to Social Security. The amount you receive depends largely on your years of service and your estimated Social Security benefit.

Before you retire, estimate your monthly income with and without the supplement, and consider how extra earnings or age changes might affect that. Planning ahead can help ensure a smoother transition and avoid income gaps.

Frequently Asked Questions

The formula is: (Years of FERS civilian service ÷ 40) × your estimated Social Security benefit at age 62. For example, a retiree with 28 years of service and an estimated Social Security benefit of $1,800/month would receive approximately $1,260/month. You can find your estimated benefit by logging into your account at SSA.gov.

The 2026 earnings limit is $24,480, up from $23,400 in 2025. If your earned income exceeds this amount, your supplement is reduced by $1 for every $2 over the limit. Only wages and self-employment income count toward the limit — TSP withdrawals, pension payments, and investment income do not.

No. The FERS supplement and Social Security are separate benefits. The supplement is designed to replace Social Security income during the gap between your early retirement date and age 62. You cannot receive both at the same time — the supplement ends automatically when your Social Security eligibility begins.

Yes, but your earnings may reduce it. If your wages or self-employment income exceed $24,480 in 2026, your supplement is reduced by $1 for every $2 above that amount. If your post-retirement earnings are high enough, the supplement could be reduced to zero entirely.

It stops. The supplement ends at the end of the month before you turn 62, even if you have not yet applied for Social Security. OPM stops payment automatically — no action is required from you, but you should plan for this income gap well before your 62nd birthday.

No. The FERS supplement is not considered earned income for purposes of the earnings test. It is also not subject to Social Security or Medicare (FICA) taxes. However, it is taxable as ordinary federal income and must be reported on your federal tax return.

Yes. The FERS annuity supplement is taxable as ordinary federal income. It is not subject to FICA taxes. State tax treatment varies — some states fully exempt federal retirement income while others tax it as ordinary income. Check your state’s rules before you retire.

Possibly. The House passed H.R. 1 in 2026, which would eliminate the FERS supplement for certain employees starting January 1, 2028. The bill is currently in the Senate. Federal employee unions are actively lobbying against it. This page will be updated as the legislation develops.

Yes. Law enforcement officers, firefighters, and air traffic controllers can retire as early as age 50 with 20 or more years of qualifying service and begin receiving the supplement immediately. They are also exempt from the earnings test until they reach their standard Minimum Retirement Age (typically 57), which is a significant advantage over regular FERS employees.

Follow these three steps: First, log into SSA.gov and find your estimated Social Security benefit at age 62 — use the age 62 figure, not the full retirement age amount. Second, count your years of FERS-covered civilian service (military time generally does not count unless formally deposited). Third, apply the formula: years of service divided by 40, multiplied by your estimated Social Security benefit at 62. OPM will calculate the official amount when you file for retirement.

Will the FERS supplement be eliminated?

I have many clients who work within the federal government and have retirement plans such as the Federal Employees Retirement System (FERS) through their employer. Many federal employees opt for early retirement, utilizing annuity benefits to supplement their income in retirement, in addition to Social Security.

Aamir M. Chalisa, MBA, LUTCF, MDRTGeneral Manager at Futurity First Insurance GroupAamir M. Chalisa is a seasoned financial services leader with over 30 years of experience in insurance, wealth management and retirement planning. As General Manager of Futurity First Insurance Group’s Oak Brook branch, he oversees one of the company’s top-performing teams. Aamir has held leadership roles at MetLife, Prudential and Nationwide and is a Million Dollar Round Table (MDRT) qualifier, recognized for his expertise in life and annuity sales and commitment to helping clients achieve lasting financial security.