What Happened with Silicon Valley Bank?

On March 10, 2023, the Federal Deposit Insurance Corporation and the California Department of Financial Protection and Innovation took over Silicon Valley Bank (SVB), the 16th largest bank in the U.S. The government intervened because SVB, which serves an array of tech start-ups, founders and venture capitalists, was unable to meet its depositors’ demands for their money. On March 12, 2023, after a weekend of high anxiety for SVB depositors, the FDIC guaranteed all the bank’s deposits, providing large depositors with protection above the $250,000 FDIC limit ($500,000 for joint accounts). The pronouncement is underpinned by the systemic risk exception, a legal clause that permits the federal government to implement extreme measures to stem nationwide banking crises. The following day, all insured and uninsured deposits and substantially all assets of SVB were transferred to a newly created, full-service FDIC-operated bridge bank. All the failed bank’s depositors were granted full access to their money, and normal banking operations resumed — with no interruption to online banking, check clearing, ATM processing, customer service or loan servicing activities. Incidentally, as part of the FDIC takeover, SVB’s senior management team was terminated. Moreover, while all depositors were granted full protection, SVB’s shareholders and certain unsecured debtholders received no protection.Did You Know?

A bridge bank is a temporary structure designed to bridge the gap between the failure of a bank and the time until the FDIC can stabilize the institution and implement an orderly resolution.

Additional Government Action

Alongside the guarantee for SVB depositors, the Federal Reserve introduced a controversial lending facility that allows all eligible banks to take collateral-based loans from the Federal Reserve using the par values of their bonds, rather than the market values — which have been beaten down by rising rates. Essentially, this is like you taking out an auto loan for $20,000 on a car that is only worth $15,000. The $5,000 difference is an unjustified influx of capital that you can use to invest and accumulate interest. It is economically nonsensical, and it encourages risk-taking and inflation — the very thing the Federal Reserve has been trying to curb with its aggressive rate hikes. The Federal Reserve rationalizes the lending facility as a precautionary measure to make sure banks have the means to meet the needs of their depositors. However, the liquidity injection into our financial system runs counter to the monetary tightening actions the Fed has been implementing since early 2022. It seems like a very illogical and unnecessary measure — unless the SVB failure is just the tip of the iceberg.Signature Bank

The FDIC takeover of New York-based Signature Bank on March 12, 2023, suggests SVB’s failure could be only the beginning. The SVB collapse, coupled with Signature’s heavy entrenchment in the cryptocurrency industry, seems to have been too much for Signature’s depositors to stomach. They made a panicked run on the bank’s deposits on March 10, 2023, necessitating regulatory intervention.Why Did the Silicon Valley Bank Failure Happen?

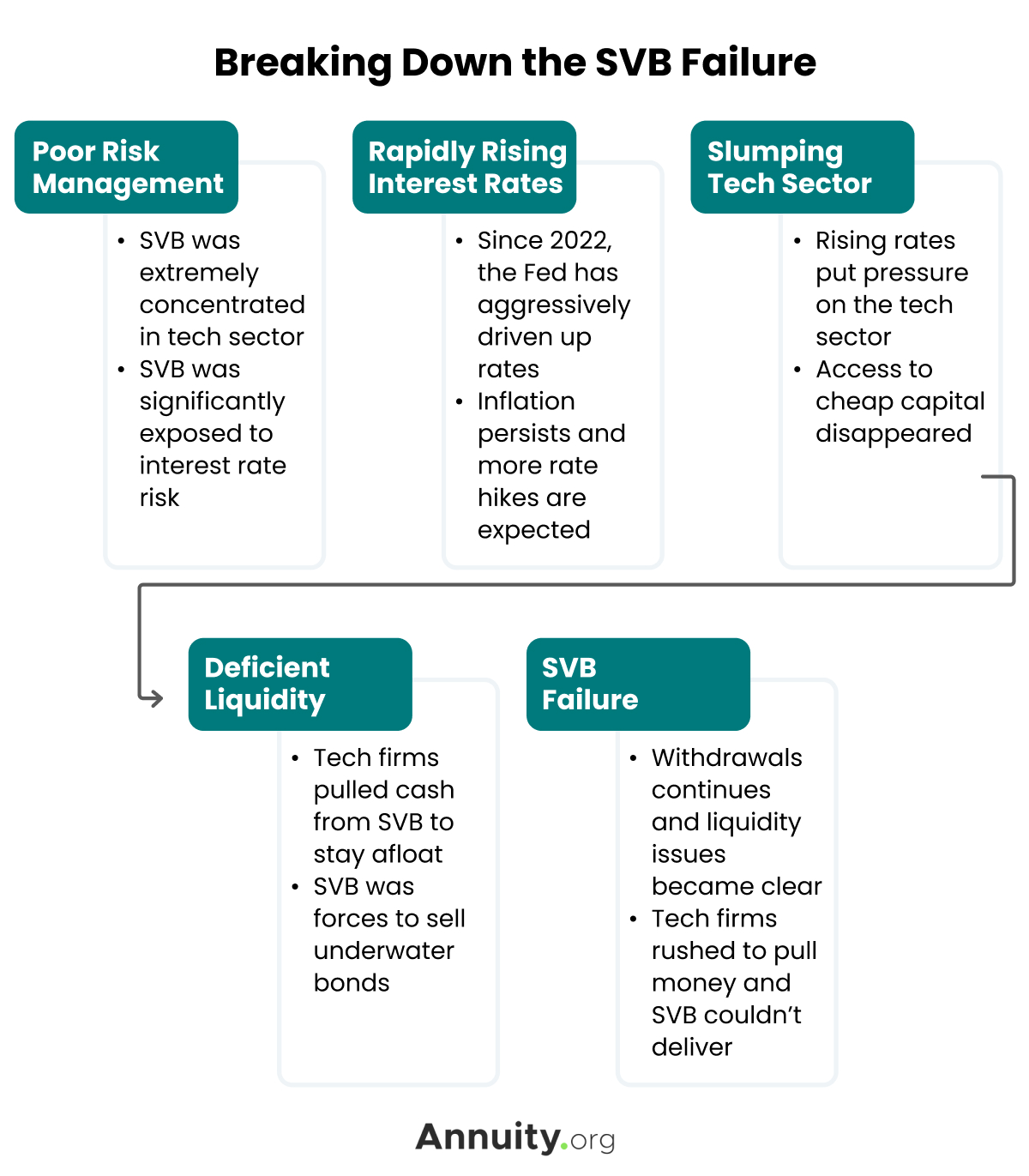

During the post-COVID-19 years of easy money and booming markets, Silicon Valley tech firms and venture capitalists were flush with cash and deposited a lot of it at SVB. The bank used some of the money to make loans, but it also invested heavily in interest-rate-sensitive, long-term bonds. Everything was going fine — until the end of 2021. Then, the Federal Reserve began aggressively driving up interest rates to combat soaring inflation. Higher rates seriously pressured the tech industry, drying up firms’ access to cheap capital. They also significantly depreciated the value of SVB’s long-term bond holdings, a byproduct of the inverse relationship between interest rates and bond prices.Did You Know?

When interest rates fall, bond prices rise. Conversely, when interest rates rise, bond prices fall. The inverse relationship is most pronounced for long-term bonds. This is known as interest rate risk.

Did You Know?

In the weeks leading up to the SVB crisis, bank executives sold millions of dollars of SVB stock. Then, hours before the FDIC took over SVB, the institution made bonus payouts to its employees. This sounds like the makings of an “American Greed” episode.

How Have Markets Responded?

As a result of the FDIC takeover, SVB’s stock plummeted by over 60%. More broadly, financial stocks have experienced heightened volatility, with several regional banks experiencing notable downward price pressure. Equity markets continue to react to the developing news, and more volatility is anticipated. Speculation around what the Federal Reserve may do at its March meeting is fanning the flame. In bond markets, U.S. Treasury yields for all tenures declined on March 13, 2023, a classic “flight to quality” effect caused by anxious investors reacting to economic uncertainty. The most significant declines were associated with the one-, two- and three-year tenures, all of which climbed higher on March 14, 2023, and declined notably on March 15, 2023.How Will the Silicon Valley Bank Failure Impact Me?

Despite the government’s unprecedented and, arguably, unnecessary actions, I do not believe we are facing a 2008-like banking crisis. Moreover, I do not think we are going to experience the widespread bank failure contagion many financial podcasters and prognosticators are circulating. The SVB failure is attributable to extremely poor risk management, as evidenced by the bank’s tremendously concentrated book of business and significant exposure to interest rate risk. That said, it is natural to be unnerved by the SVB failure and the subsequent Signature Bank collapse. Take the following steps to safeguard your money and put your mind at ease:- Assess the size of the balances you have at your banks. Make sure you do not have more than $250,000 at any single bank ($500,000 for joint accounts). If necessary, implement an FDIC-insurance cash sweep program that automatically spreads your money across multiple banks, ensuring 100% of your money is insured by the FDIC.

- Do not execute any knee-jerk sales of your stocks, bonds and other investments. Discuss your investment strategy with your financial advisor and rationalize your asset allocation. Make sure it is still appropriate, given your investment objectives and time horizon. If you do not have an advisor, I suggest you look into getting one, perhaps, a low-cost robo-advisor.

- If you have annuities and/or life insurance products and are worried about the financial condition of the issuing insurance companies, assess their AM Best Financial Strength Ratings. The strongest insurers have a rating of at least “A- (Excellent).” These top-tier companies are in superb financial condition and can be relied upon to meet their contractual obligations during good and bad economic environments.

- If you have cash you want to put to work, but only in a conservative way that gives you the highest probability of keeping pace with inflation, I recommend I bonds. These are a type of inflation-protected security issued by the U.S. Department of the Treasury. They are non-marketable, high-quality debt instruments that offer a fixed rate of return plus a variable rate indexed to the Consumer Price Index (CPI).